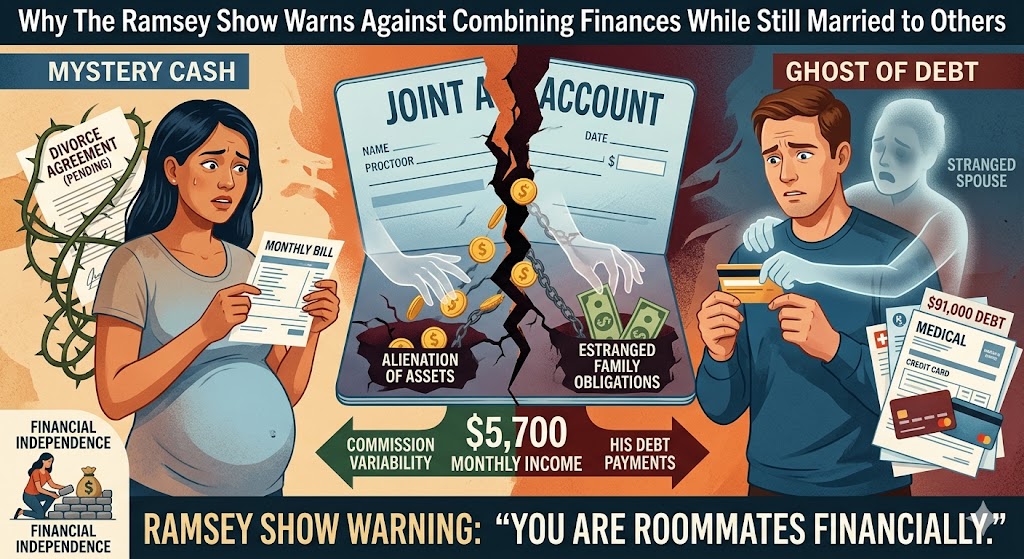

Breaking Texas News: The intersection of romance and personal finance is often a treacherous path, but adding the complication of unresolved legal marriages creates a financial minefield that can devastate one’s future. On a recent episode of The Ramsey Show, aired Friday, April 11, 2026, financial experts Rachel Cruze and John Delony issued a stark warning to listeners: Never combine your finances with a partner if one or both of you are still legally married to other people.

Using a harrowing call from a listener named Grace as a case study, the hosts dissected the emotional, legal, and mathematical reasons why “playing house” financially before a divorce is finalised is a recipe for disaster.

The Story of Grace: A Case Study in Financial Vulnerability

Grace, calling from Colorado, presented a scenario that John Delony described as “terrifyingly common yet incredibly dangerous.” Grace and her partner have been living together and functioning as a single financial unit since last summer. However, there is a major legal hurdle: both are still technically married to their previous spouses.

Grace’s situation is further complicated by several high-stress factors:

- Pregnancy: Grace is newly pregnant, adding a ticking clock to her need for financial stability.

- Massive Debt: The couple shares a staggering $91,000 in combined debt.

- Unstable Income: Grace works on commission, with her monthly take-home pay fluctuating between a $2,500 base and $4,000.

- Legal Stagnation: Her partner has not yet filed for divorce because he claims he cannot afford the $5,000 attorney’s retainer fee.

- External Obligations: Her partner has two children with his estranged wife, creating a permanent legal and financial link to his past marriage.

With a combined after-tax income of approximately $5,700, the couple is living paycheck to paycheck, struggling to breathe under the weight of debt while floating in a legal limbo.

“You Are Roommates”: The Delony Reality Check

The core of the advice from The Ramsey Show co-hosts centred on a hard truth: without a marriage certificate between the two of them, and with marriage certificates still active with other people, Grace and her partner have no legal standing as a couple.

“You are roommates financially. You have to think about it that way,” Delony told Grace.

The Legal Risks of “Intermingling”

When you combine bank accounts, pay each other’s credit card bills, or co-sign for loans while still legally married to someone else, you are inviting the “ghosts” of previous marriages into your current wallet.

- Divorce Court Scrutiny: In many jurisdictions, a judge or an estranged spouse’s attorney can look at bank statements during a divorce discovery phase. If a partner is using “joint” money to pay for a new girlfriend’s car or rent, that money could be classified as “dissipation of marital assets,” forcing the partner to pay that money back to the estranged spouse.

- Asset Seizure: If Grace’s partner’s estranged wife wins a judgment for child support or alimony, and that partner’s name is on Grace’s bank account, those funds—including Grace’s hard-earned commissions—could be frozen or seized.

- No Inheritance Rights: If Grace’s partner were to pass away unexpectedly, his assets (including half of any joint accounts) would likely legally flow to his “legal” wife and children, leaving Grace—and her unborn child—with nothing.

The “Commission Trap” and Budgeting for One

Rachel Cruze highlighted the specific danger of Grace’s income structure. Because Grace’s income is commission-based, her “floor” is only $2,500.

“Your variability leaves zero room for error,” Cruze noted. When you combine an unstable income with someone else’s $91,000 debt and their unresolved legal fees, you aren’t just helping a partner; you are drowning with them.

Cruze and Delony’s primary recommendation was for Grace to uncombine immediately:

- Stop paying his bills: He is responsible for his $91,000 debt and his $5,000 divorce retainer.

- Separate the accounts: Grace needs a “Grace-only” account where her commissions land.

- The Roommate Budget: They should split the rent and utilities 50/50 (or proportionally), but Grace must prioritise her own savings and the upcoming costs of her pregnancy.

Why the “Retainer Fee” Excuse is a Red Flag

A poignant moment in the show occurred when the hosts addressed the partner’s inability to pay the $5,000 divorce retainer. Delony was blunt: if the partner can’t find a way to scrape together $5,000 to end his previous marriage, he isn’t ready to be in a new financial partnership.

By Grace helping him with his daily expenses, she is essentially “subsidising” his choice to remain legally married to another woman. The hosts urged Grace to realize that her partner’s divorce costs are his personal responsibility. Taking on that burden only delays his growth and increases her risk.

Practical Steps for Couples in “Legal Limbo”

For those who find themselves in a committed relationship while waiting for a divorce to finalise, The Ramsey Show suggests a strict “Business Partner” approach to money:

1. Maintain Radical Separation

Keep all credit cards, car titles, and savings accounts in individual names. Do not put a partner’s name on your lease or mortgage if it can be avoided.

2. Use Digital Payment Apps for Household Costs

Instead of a joint account, use apps like Venmo or Splitwise to handle groceries and utilities. This creates a clear paper trail showing that you are paying your share, not merging your lives.

3. Focus on the “Four Walls”

Grace was advised to focus strictly on her “Four Walls”—Food, Utilities, Shelter, and Transportation—based on her $2,500 baseline income. Anything extra should be saved for the baby, not used to pay down a partner’s pre-existing debt.

The Emotional Toll of Financial Infidelity and Entanglement

The show also touched upon the concept of Financial Infidelity. While Grace and her partner are open about their debts, they are committing a form of financial self-sabotage by ignoring the legal realities of their situation.

Cruze noted that many Americans are hesitant to reveal the full extent of their financial struggles, which leads to “straining relationships.” In Grace’s case, the strain isn’t just the debt—it’s the lack of a clear boundary between her future and her partner’s past.

Conclusion: Protection Over Proximity

The overarching message from Rachel Cruze and John Delony was clear: Love is not a legal shield. While Grace and her partner may feel like a family, the law sees two people who are still bound to other households. Until the “Decree Absolute” is signed and the ink is dry on the divorce papers, combining finances isn’t an act of trust—it’s an act of extreme financial negligence.

For Grace, the path forward is one of independence. By separating her finances, she isn’t just protecting her paycheck; she is protecting her peace of mind and the future of her child. As Delony summarised, “You can’t build a house on a foundation that someone else still owns.”

Top stories you may also like

-

Microsoft Corporation (US5949181045): Is AI Integration Now the Real Test for Sustained U.S. Market Dominance?

WALL STREET, NY — As the Nasdaq remains the focal point for global tech valuation, Microsoft Corporation (US5949181045)

-

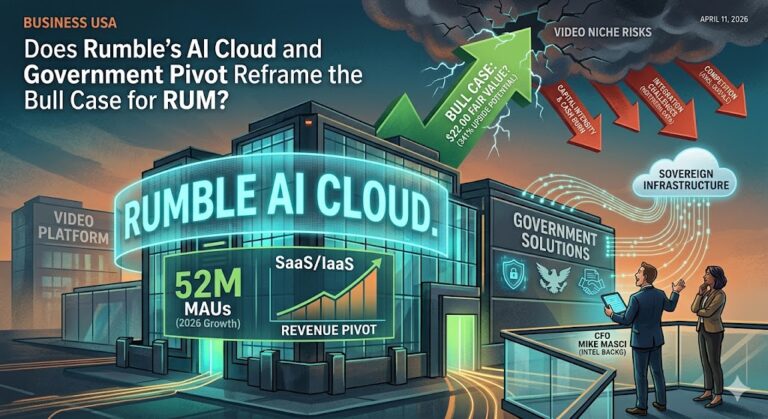

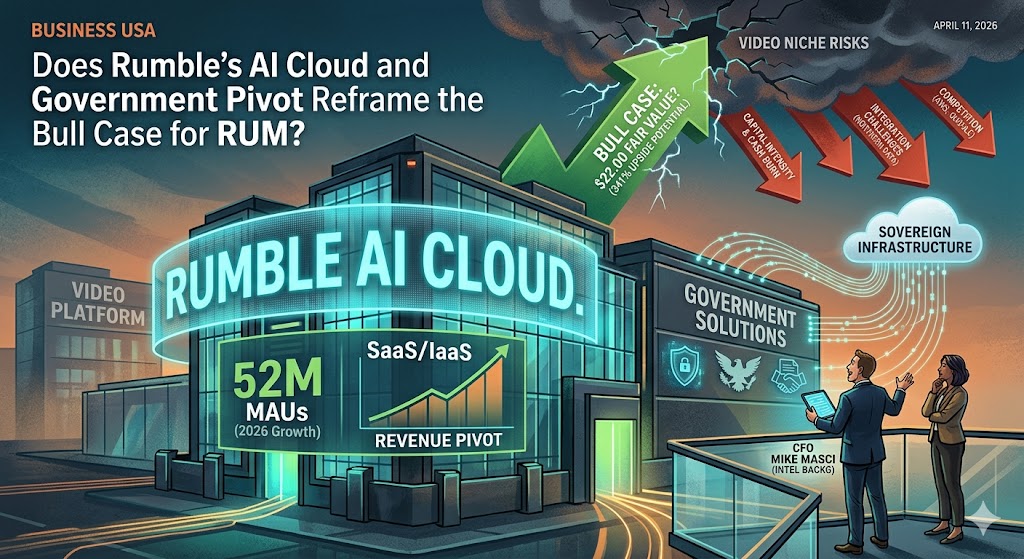

Business USA : Does Rumble’s AI Cloud and Government Pivot Reframe the Bull Case for RUM?

The digital landscape of 2026 is being redrawn by two massive forces: the insatiable demand for AI-driven compute

-

Alaska Airlines indicates Major West Coast Growth with $135 Million Portland Maintenance Hub

PORTLAND, OR — Read on this USA latest news website all about the Alaska Airlines breaking updates. What