The digital landscape of 2026 is being redrawn by two massive forces: the insatiable demand for AI-driven compute power and the increasing necessity for “sovereign” digital infrastructure. At the 38th Annual Roth Conference, held on April 11, 2026, Rumble Inc. (RUM) leadership laid out a strategic roadmap that attempts to position the company at the intersection of both.

Once viewed strictly as a “free-speech” alternative to YouTube, Rumble is aggressively pivoting toward an AI-powered cloud infrastructure model and deepening its ties with government clients. But as the stock sits in a volatile position, investors are asking: Is this a genuine transformation into an enterprise powerhouse, or a capital-intensive gamble that risks the company’s financial stability?

The Growth Trajectory: From Video Niche to Infrastructure Scale

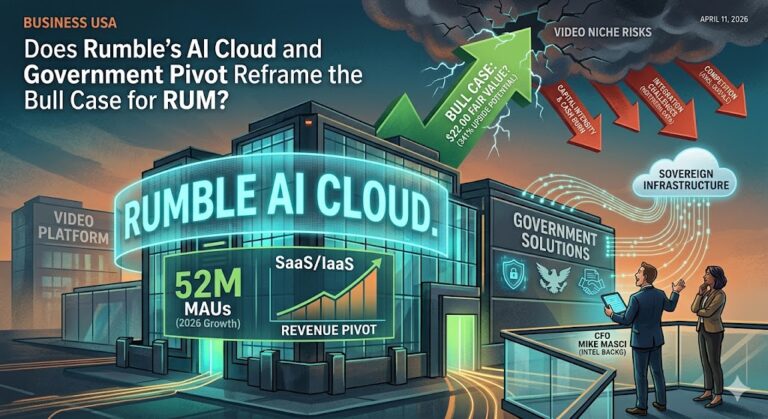

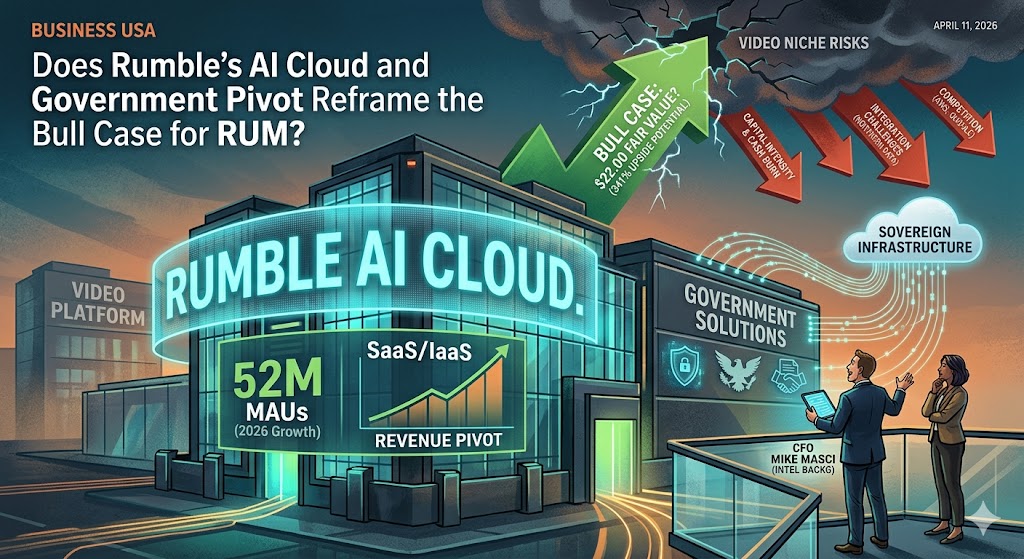

Rumble’s transition has been nothing short of rapid. Management highlighted a staggering leap in Monthly Active Users (MAUs)—moving from a mere 1 million in 2020 to 52 million in early 2026. However, the Roth Conference presentation made it clear that MAUs are no longer the only metric that matters.

The company is repositioning itself as a broader infrastructure provider. This shift is centred on:

- AI Cloud for SMBs: Providing small and medium-sized businesses with AI-powered tools that were previously only accessible to tech giants.

- Government Relationships: Expanding its cloud footprint to serve government agencies that require high-security, politically neutral, and censorship-resistant hosting environments.

By moving beyond video, Rumble aims to tap into the high-margin world of SaaS (Software as a Service) and IaaS (Infrastructure as a Service), potentially insulating itself from the whims of the volatile digital advertising market.

The Mike Masci Factor: A Strategic Appointment

Perhaps the most significant signal of Rumble’s intent was the appointment of Mike Masci as CFO. Masci isn’t a traditional media executive; his background at Intel focused on AI, cloud infrastructure, and M&A.

Masci’s presence is seen as a direct catalyst for the potential acquisition of Northern Data. If successful, this move would provide Rumble with the raw hardware power—high-end GPUs—necessary to compete in the generative AI space. His expertise in complex integrations suggests that Rumble is moving away from being a “scrappy startup” toward becoming a calculated, enterprise-grade player.

The Bull Case: A 341% Upside?

For those with a high risk tolerance, the “Bull Case” for Rumble is tantalizing. Some analyst models, including those featured on Simply Wall St, project a fair value of $22.00 per share. Compared to current trading prices, this represents a massive 341% upside.

To reach this lofty goal, the bull narrative hinges on several aggressive forecasts:

- Revenue Growth: Projecting $723.4 million in revenue by 2029.

- Profitability Pivot: Turning a current $81.8 million loss into an $11.8 million profit within the next three years.

- 93% Yearly Growth: This requires Rumble to maintain a near-triple-digit annual growth rate in its cloud division to offset the heavy costs of infrastructure.

The Bear Case: Cash Burn and Capital Intensity

Despite the optimism, the “Bear Case” remains grounded in the harsh reality of capital expenditures (CapEx). Building AI clouds is expensive.

“To own Rumble, you need to believe it can evolve while managing ongoing losses,” the Simply Wall St review notes.

The biggest risk factors identified include:

- Heavy Spending: Management is currently prioritizing growth and infrastructure over adjusted EBITDA breakeven.

- Integration Risks: Acquiring hardware companies like Northern Data involves massive integration challenges that could prolong unprofitability.

- Competitive Pressure: Rumble isn’t just fighting BitChute or X anymore; it is now entering a ring with Amazon Web Services (AWS), Google Cloud, and Microsoft Azure.

Pessimistic analysts are far more conservative, projecting only $185.6 million in revenue by 2028 with no path to profitability in sight. They argue that content-related risks and the sheer cost of AI compute will weigh far more heavily on the stock than the Roth Conference narrative suggests.

Deciding for Yourself: The “Snowflake” Analysis

Evaluating Rumble requires a balance of looking at high-level “growth stories” and digging into the granular data. Investors are encouraged to look at financial health visualizations, such as the “Snowflake” analysis, which provides a snapshot of:

- Value: Is the stock currently trading below its intrinsic worth?

- Future Growth: Can it hit that 93% yearly revenue target?

- Past Performance: How well has management utilized its cash in the past?

- Health: Does it have the runway to survive the current burn rate?

Conclusion: A High-Stakes Transformation

Rumble’s pivot to an AI Cloud and Government infrastructure model is a bold attempt to escape the “social media” box. By hiring Intel veterans and eyeing hardware acquisitions, management is making a play for the “Nuclear Renaissance” of AI—where energy and compute power are the new oil.

However, the road to a $22.00 fair value is paved with significant financial hurdles. Whether Rumble becomes an essential pillar of the AI revolution or a cautionary tale of over-expansion will depend on Mike Masci’s ability to balance the books while the company builds out its high-tech fortress.

FAQ: Rumble’s AI Cloud Pivot

1. Why is Rumble moving into AI Cloud services?

Rumble wants to diversify its revenue beyond video advertising. By offering cloud infrastructure, they can serve enterprise and government clients who need secure, independent hosting for AI applications.

2. Who is Mike Masci and why does his appointment matter?

Mike Masci is the new CFO. His experience in AI and M&A at Intel suggests that Rumble is serious about acquiring hardware and scaling its technical infrastructure to compete with major cloud providers.

3. Is Rumble profitable?

No. As of April 2026, Rumble is still operating at a loss (approx. -$81.8 million) as it prioritizes infrastructure spending and growth over short-term earnings.

4. What is the “fair value” of RUM stock?

While some analysts see a fair value of $22.00 based on aggressive 2029 projections, others warn that the stock could be worth less than half its current price if it fails to manage its cash burn.

5. What is the biggest risk to RUM investors?

The primary risk is cash burn. Building an AI cloud requires massive capital investment, and there is no guarantee that the company will reach EBITDA breakeven before it runs out of liquidity.

For more in-depth stock analysis and elite penny stock lists balancing risk and reward, visit Simply Wall St’s full Rumble research report.