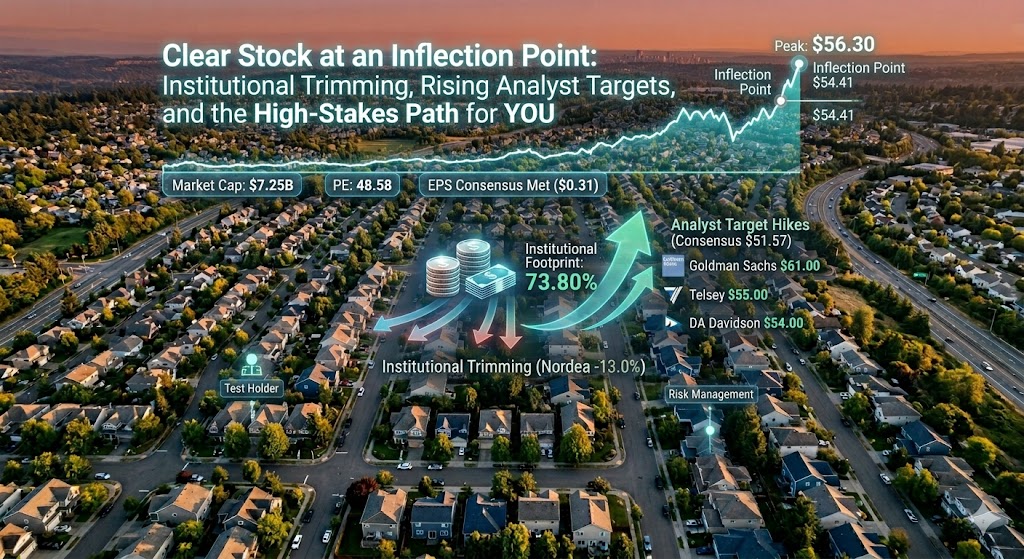

NEW YORK — CLEAR Secure, Inc. (NYSE: YOU), the biometric identity giant known to millions of travelers simply as “Clear,” has reached a critical structural crossroads. As of March 26, 2026, the company finds itself caught in a tug-of-war between diverging market forces: institutional investors are beginning to trim their exposure, while Wall Street analysts are aggressively hiking price targets following a quarterly earnings report that met expectations but signaled shifting fundamentals.

With the stock currently trading near its 52-week high of $56.30, the question for investors is whether the current momentum is sustainable or if the “inflection point” signals an impending period of consolidation.

The Institutional Shift: Strategic Rebalancing or a Warning Sign?

One of the most significant developments in the recent quarter is the change in institutional positioning. Nordea Investment Management AB, a major player in the space, recently disclosed in a filing with the U.S. Securities and Exchange Commission that it trimmed its position in CLEAR Secure by 13.0%.

Nordea sold 47,676 shares, leaving it with a remaining stake of 319,634 shares valued at approximately $11.28 million. While a 13% reduction isn’t necessarily a vote of no confidence, it highlights a broader trend of “profit-taking” as the stock approaches its overhead resistance levels.

Key Institutional Ownership Stats:

- Total Institutional Ownership: 73.80%

- Market Capitalization: $7.25 Billion

- Beta: 1.13 (indicating slightly higher volatility than the broader market)

Despite Nordea’s exit, the stock retains a “sticky” institutional base. Firms like Geneos Wealth Management Inc. and Advisors Asset Management Inc. have recently initiated or increased their positions. However, when 73.8% of a company is owned by institutions and hedge funds, even minor rebalancing acts can cause outsized swings in the share price.

Analyst Sentiment: Higher Targets vs. Cautious Ratings

While some institutions are trimming, the analyst community is busy rewriting their price objectives. The recent wave of revisions suggests a “bullish divergence”—where price targets are rising faster than actual ratings.

| Financial Institution | New Price Target | Previous Target | Rating |

|---|---|---|---|

| The Goldman Sachs Group | $61.00 | N/A | Buy |

| Telsey Advisory Group | $55.00 | $45.00 | Outperform |

| DA Davidson | $54.00 | $46.00 | Buy |

| JPMorgan Chase & Co. | $47.00 | $42.00 | Overweight |

Despite these individual jumps, the consensus rating remains a “Hold” with a consensus price target of $51.57. This gap exists because firms like Weiss Ratings recently downgraded the stock from a “Buy” to a “Hold,” citing concerns over valuation. With a PE ratio of 48.58, Clear Stock is currently priced for perfection, leaving little room for error in the coming months.

Fundamental Health: Hitting the Consensus Mark

The company’s latest earnings report, released on February 25th, served as a validation for some and a caution for others. Clear reported an Earnings Per Share (EPS) of $0.31, perfectly matching the consensus estimate.

Quarterly Financial Highlights:

- Revenue: $240.75 million (beating the $235.66 million estimate).

- Year-over-Year Revenue Growth: +16.7%.

- Net Margin: 12.12%.

- Return on Equity (ROE): 70.08%.

While hitting the $0.31 EPS mark is positive, investors are closely watching the year-over-year comparison. In the same quarter last year, the business posted a much higher $0.91 EPS. This sharp decline in earnings, despite growing revenue, indicates that the company is spending heavily on expansion, technology integration, and customer acquisition.

Technical Analysis: Trading at the Edge

From a technical perspective, YOU is currently in “overbought” territory relative to its historical averages. The stock opened at $54.41 in the latest session, trending up 1.6%.

The massive gap between the current price and its moving averages is the primary concern for technical traders:

- Current Price: ~$54.41

- 50-Day Moving Average: $39.59

- 200-Day Moving Average: $36.42

When a stock trades this far above its 200-day moving average, it often experiences a “mean reversion”—a pull-back toward the average. For Clear Stock to sustain these levels, it will need another catalyst, likely in the form of a strategic partnership or a surprise uptick in subscription renewals.

The Next Test for “YOU”

The “next test” for Clear Secure is structural. As institutional filing periods approach, the market will see if the Nordea trim was an isolated incident or the start of a mass exodus to lock in gains.

If the stock can hold the $54.00 support level despite institutional selling, it validates the $61.00 bull case set by Goldman Sachs. If it fails, the 50-day moving average near $40.00 becomes the likely destination for a landing.

For investors, the current inflection point suggests that while the company’s growth story remains intact (evidenced by the 16.7% revenue jump), the stock’s price may have moved ahead of its immediate earnings potential.

Would you like me to analyze how Clear’s recent partnership expansions might influence the next quarter’s revenue targets?