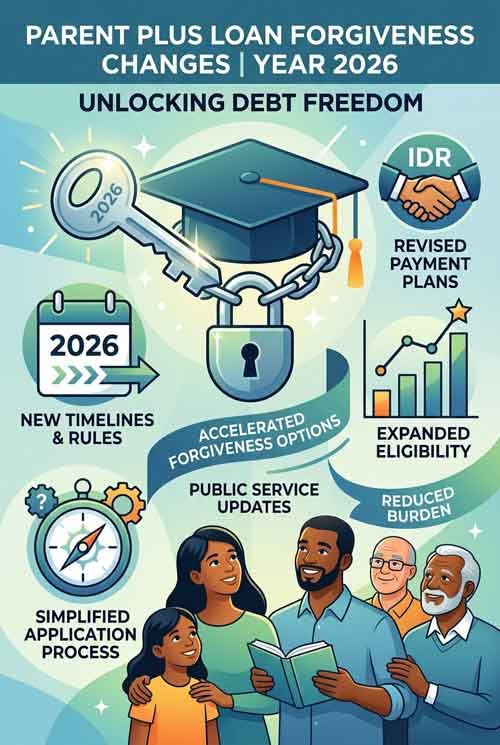

USA Parent PLUS Loan Forgiveness Changes 2026: Check New Rules, Eligibility & Repayment Guide

Latest US financial news: This news article delivers details of the USA Parent PLUS loan forgiveness new rules, eligibility and repayment guide. Along with this, also know about whether Parent PLUS loans can be forgiven after 20 years and other related breaking news.

Millions of American parents have borrowed federal Parent PLUS Loans to help their children pay for college. While these loans have helped families bridge the gap between financial aid and tuition costs, they have also created long-term debt for many borrowers.

Over many years, the federal student loan system has experienced several policy updates. As a result, many borrowers have questions about parent PLUS loan forgiveness changes, repayment plans, eligibility rules, and whether forgiveness programs are still available.

The latest big news is that Parent PLUS borrowers still have options. However, the rules differ from those for Direct Subsidised and Direct Unsubsidized Loans. Understanding those differences can help borrowers avoid costly mistakes and choose the right repayment strategy.

This guide explains the latest Parent PLUS loan forgiveness rules using verified information from the U.S. Department of Education and Federal Student Aid.

Parent PLUS Loans – What’s inside?

A Parent PLUS Loan is a federal loan available to parents of dependent undergraduate students enrolled at eligible colleges or universities.

Unlike student loans that belong to the student, Parent PLUS Loans are the legal responsibility of the parent who borrowed the money. Even if the student graduates, finds a great job, or promises to help repay the loan, the parent remains legally responsible for repayment.

Key features include:

- Fixed interest rate set annually by Congress

- Federal borrower protections

- Multiple repayment options

- Access to certain federal forgiveness programs

- No annual or aggregate borrowing limits beyond the school’s cost of attendance

What Are the Recent Parent PLUS Loan Forgiveness Changes?

The phrase parent plus loan forgiveness changes mainly refers to recent adjustments in repayment programs rather than the complete elimination of forgiveness opportunities.

Several federal policy changes have affected Parent PLUS borrowers.

1. SAVE Repayment Plan Is Not Available

One of the biggest changes is that Parent PLUS borrowers cannot directly enrol in the SAVE (Saving on a Valuable Education) repayment plan. SAVE replaced the former REPAYE plan for many federal borrowers, but Parent PLUS Loans were never eligible for REPAYE or SAVE. Borrowers hoping for lower monthly payments under SAVE must understand that this option does not currently apply to Parent PLUS Loans.

2. Income-Contingent Repayment Still Exists

Parents who consolidate their Parent PLUS Loans into a Direct Consolidation Loan may become eligible for the Income-Contingent Repayment (ICR) Plan.

ICR calculates monthly payments based on income and family size.

Although ICR often produces higher payments than SAVE, it remains the primary income-driven repayment option available for Parent PLUS borrowers.

3. Public Service Loan Forgiveness Remains Available

Parents working full-time for qualifying government employers or eligible nonprofit organisations may still qualify for Public Service Loan Forgiveness (PSLF).

To receive forgiveness, borrowers generally must:

- Work full-time for a qualifying employer

- Make 120 qualifying monthly payments

- Repay under an eligible repayment plan, usually ICR after consolidation

- Hold eligible Direct Loans

This program continues to provide one of the most valuable forgiveness opportunities for Parent PLUS borrowers.

Can Parent PLUS Loans Be Forgiven?

Yes.

Parent PLUS Loans may qualify for forgiveness under specific federal programs. However, eligibility depends on the borrower’s employment, repayment history, and loan type.

Common forgiveness pathways include:

- Public Service Loan Forgiveness

- Income-Contingent Repayment forgiveness after the required repayment period

- Total and Permanent Disability Discharge

- Death discharge

- School closure discharge (in limited circumstances)

- Borrower defence to repayment (when applicable)

Each program has different eligibility rules.

Income-Driven Repayment and Parent PLUS Loans

Many borrowers think that every federal loan qualifies for income-driven repayment. But that assumption is incorrect.

Parent PLUS Loans have more limited eligibility. Without consolidation, Parent PLUS Loans generally do not qualify for most income-driven repayment plans. After consolidation, borrowers may access the Income-Contingent Repayment Plan.

While this requires an extra step, consolidation can reduce monthly payments for eligible borrowers and may open the door to loan forgiveness after the required repayment period.

Public Service Loan Forgiveness How?

PSLF remains one of the strongest federal forgiveness options available.

Parents working in education, healthcare, military service, state government, local government, tribal government, or qualifying nonprofit organisations may qualify.

Examples of eligible employers include:

- Public schools

- State universities

- County governments

- Public hospitals

- Military branches

- Many nonprofit organisations with tax-exempt status

Remember, eligibility depends on the parent’s employment—not the student’s career.

That’s an important distinction many families overlook.

What About the Double Consolidation Loophole?

For years, some Parent PLUS borrowers used what’s commonly called the Double Consolidation Loophole to gain access to additional income-driven repayment plans.

Federal regulations have changed, and this strategy is being phased out.

Borrowers considering this approach should review the latest Department of Education guidance because eligibility depends on when consolidations occurred and whether regulatory deadlines apply.

Anyone planning consolidation should understand the current rules before submitting applications.

Common Misunderstandings About Parent PLUS Loan Forgiveness

Should You integrate Your Parent PLUS Loan?

Consolidation can help many borrowers, but it is not always the right choice.

Potential benefits include:

- Access to Income-Contingent Repayment

- Eligibility for PSLF when other requirements are met

- Simplified repayment with one monthly bill

Possible drawbacks include:

- Interest capitalization

- Restarting certain repayment timelines

- Loss of some borrower benefits tied to older loans

Borrowers should compare their current loan status before deciding.

How to Apply for Parent PLUS Loan Forgiveness

The process depends on the forgiveness program.

Generally, borrowers should:

- Review current loan type.

- Determine whether consolidation is needed.

- Select an eligible repayment plan.

- Certify qualifying employment if pursuing PSLF.

- Keep payment records.

- Submit required forgiveness applications when eligible.

Accurate documentation helps prevent delays.

Management tips

Paying off education debt can feel overwhelming, but a few smart habits make a difference.

Check Your Interest Rates

Understanding your loan’s interest rate helps you estimate long-term costs.

Review Your Repayment Plan Timely

Life changes. Income, retirement plans, and employment may affect the repayment option that works best for you.

Keep Your Contact Information Safe

Missing notices from your loan servicer can create unnecessary problems.

Avoid Scams activity

Unfortunately, scammers often target borrowers searching for loan forgiveness.

Remember:

- Federal loan forgiveness applications do not require expensive third-party services.

- Never pay upfront fees for guaranteed forgiveness.

- Always verify information through official federal resources.

If someone promises instant forgiveness for a fee, that’s a major red flag.

How Does It Affect Families?

According to recent US financial news. Many families borrowed Parent PLUS Loans, expecting stable repayment options.

These new policy updates have changed some of those expectations. While newer repayment plans remain not applicable for Parent PLUS borrowers, existing federal protections continue to provide meaningful relief for many households. Parents working in public service may still receive significant benefits through PSLF, while others may reduce payments through Income-Contingent Repayment after consolidation.

The key is understanding which programs actually apply to your loans.

Frequently Asked Questions FAQs

Are Parent PLUS Loans eligible for forgiveness?

Yes. Eligible borrowers may qualify through Public Service Loan Forgiveness, Income-Contingent Repayment forgiveness, disability discharge, or other federal discharge programs.

Can Parent PLUS borrowers enrol in SAVE?

No. Parent PLUS Loans are not directly eligible for the SAVE repayment plan.

Does consolidating Parent PLUS Loans help?

It can. Consolidation may provide access to Income Contingent Repayment and, in some cases, Public Service Loan Forgiveness.

Who must work for a qualifying employer under PSLF?

The parent borrower, not the student, must meet the employment requirement.

Can private Parent PLUS loans be forgiven?

Federal forgiveness programs generally do not apply to private education loans.

Conclusion

Understanding parent plus loan forgiveness changes is more important than ever for families managing college debt. While recent policy updates have limited access to some newer repayment plans, Parent PLUS borrowers still have meaningful federal options.

Thus, Borrowers who consolidate their loans may qualify for Income-Contingent Repayment, and those employed by eligible public service organisations may still benefit from Public Service Loan Forgiveness. Other federal discharge programs also remain available in qualifying situations.

Rather than relying on rumours or social media advice, review your loan details carefully, confirm your eligibility through official federal resources, and choose the repayment strategy that best fits your financial goals. A well-informed decision today can make loan repayment more manageable in the years ahead.

Join the Trump Parents Plus loan forgiveness forum discussion to learn more about this and what parents should know

Trusted Sources

- U.S. Department of Education – Federal Student Aid: https://studentaid.gov

- Federal Student Aid – Income-Driven Repayment Plans: https://studentaid.gov/manage-loans/repayment/plans/income-driven

- Federal Student Aid – Public Service Loan Forgiveness (PSLF): https://studentaid.gov/manage-loans/forgiveness-cancellation/public-service

- U.S. Department of Education – Direct Consolidation Loans: https://studentaid.gov/loan-consolidation

READ ALSO BREAKING NEWS IN AMERICA TODAY BELOW

-

US Country Singer Zach John King HALT Tour After his father death. Breaking News Now

Breaking Now : US Country music artist Zach John King has announced that he is stepping away from touring following the sudden death of his father, John King. In a heartfelt social media post shared on July 14, King revealed that his father had died unexpectedly the previous Friday. Alongside a photo of the two…

-

Canada Wildfires and U.S. Air Quality: How Smoke Is Affecting Millions Across North America

Boston today news :Canada Wildfires smoke has become an increasingly familiar part of summer for many communities across North America. Even people who live hundreds or thousands of miles from an active wildfire can experience hazy skies and unhealthy air. Advances in weather forecasting and air quality monitoring have helped people prepare for these events,…

-

PayPal stock share bounce After Reported Acquisition Offer

PayPal shares surged on Wednesday after reports claimed that payments company Stripe and private equity firm Advent International submitted a joint bid to acquire the digital payments company. The reported offer values PayPal at approximately $53 billion, making it one of the largest potential fintech acquisitions in recent years. Investors welcomed the news, pushing PayPal…